Anker Brand Research Report

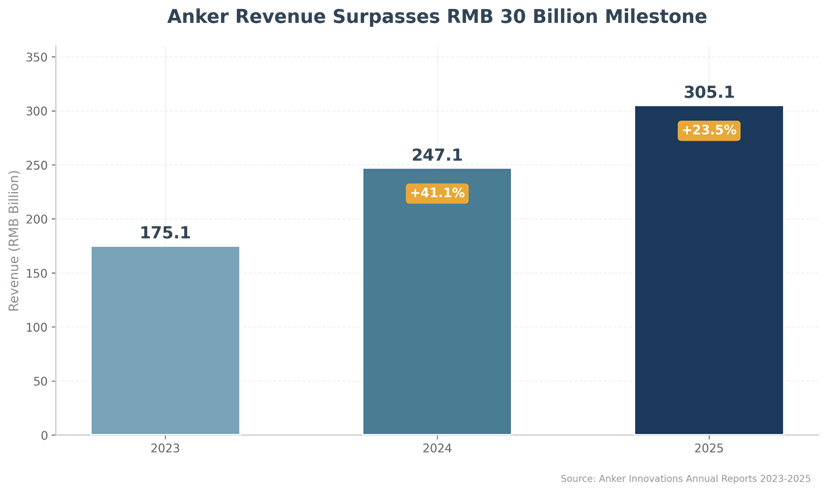

Anker(Amazon storefront) Innovations, a global leader in charging and energy storage, achieved operating revenue of RMB 30.514 billion in 2025, representing a year-on-year increase of 23.49%, surpassing the RMB 30 billion milestone for the first time. Net profit attributable to shareholders reached RMB 2.545 billion, up 20.37% YoY, with weighted average return on equity (ROE) improving to 26.10%, demonstrating sustained robust profitability.

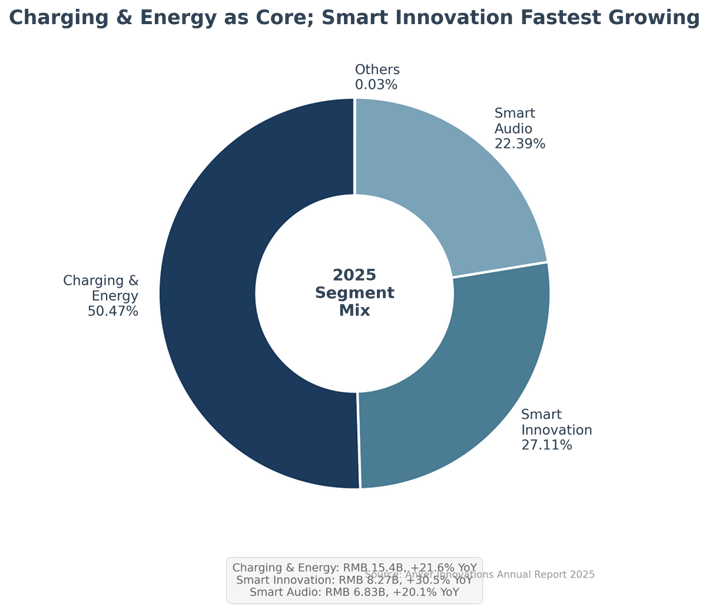

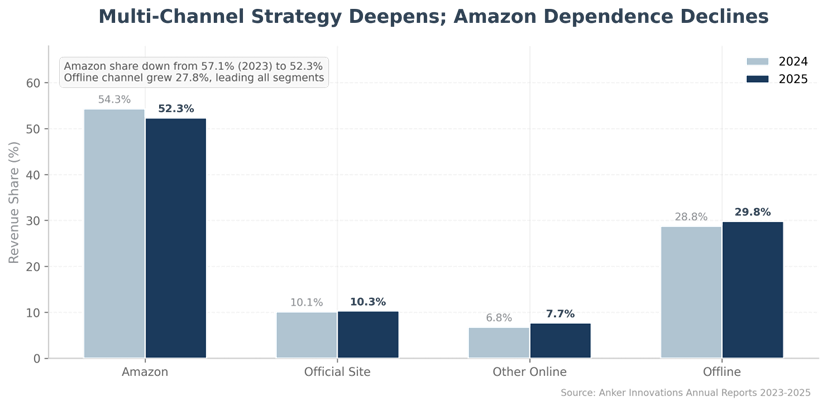

The company continues to execute its "Shallow-Sea Strategy," now organized around three core brands: Anker (charging and energy), Soundcore (smart audio), and Eufy (smart home). The charging and energy segment contributed 50.47% of core revenue, while smart innovation grew at 30.53%, emerging as the company's second growth curve. Global expansion delivered strong results: European revenue surged 43.38%, offline channel share rose to 29.78%, and Amazon dependence declined from 57.1% in 2023 to 52.3%.

On the AI front, the company's "All in AI" initiative since 2023 has yielded commercialized products across smart security, energy management, and audio translation. Anker holds a commanding 14.8% share of the global GaN charger market, with the GaN power semiconductor market projected to grow at a 31.8% CAGR to USD 8 billion by 2035, providing substantial long-term runway.

Anker Innovations was founded in 2011 by Steven Yang, a 2008 graduate of Peking University's Computer Science department who subsequently worked at Google as a software engineer on the Chrome browser's early stability testing. This experience instilled a core belief: "Stability may not be developers' top priority, but it is what users care about most." This first principle has guided Anker's product philosophy for over a decade.

In 2011, Yang left Google to start Anker in China. Rather than chasing trends like the sharing economy or blockchain, he focused on what seemed almost trivial: a power bank that would not overheat or malfunction. "We don't aim to be the newest or the biggest; we aim to be the most stable." The company has consistently kept advertising spend below 10% of revenue, relying on product excellence rather than paid acquisition to drive growth.

Key Milestones

|

Year |

Key Milestone |

|

2011 |

Steven Yang founded Anker; first product was an ultra-stable

power bank |

|

2016 |

Launched eufy and soundcore sub-brands; began multi-category

expansion |

|

2018 |

First to commercialize GaN (gallium nitride) technology

globally |

|

2020 |

IPO on ChiNext board; introduced the "Shallow-Sea

Strategy" |

|

2023 |

Declared "All in AI" direction; built AIME agent

platform |

|

2025 |

Revenue surpassed RMB 30 billion; brand portfolio consolidated

to three |

In 2025, Anker Innovations reported total operating revenue of RMB 30.514 billion, up 23.49% year-on-year, representing cumulative growth of 74.3% from RMB 17.507 billion in 2023. While the growth rate moderated from 41.1% in 2024 to 23.5% in 2025, this trajectory reflects a maturing yet still rapidly expanding business.

Figure 1: Anker Revenue Growth Trend 2023-2025 (RMB Billion)

On a quarterly basis, Q4 2025 revenue reached RMB 9.495 billion, accounting for 31.1% of full-year revenue and setting a new quarterly record. This aligns with the year-end consumer electronics season and the company's concentrated new product launch cycle. Operating cash flow declined 82.49% to RMB 481 million, primarily due to strategic inventory buildup and channel expansion investments.

The company focuses on three core verticals: charging and energy, smart innovation, and smart audio. In 2025, charging and energy generated RMB 15.402 billion, up 21.59% YoY and accounting for 50.47% of total revenue, maintaining its position as the core business. Smart innovation achieved RMB 8.271 billion, up 30.53% and representing 27.11% of revenue, leading all segments in growth rate. Smart audio contributed RMB 6.833 billion, up 20.05% and accounting for 22.39%.

Figure 2: 2025 Business Segment Revenue Mix

In the charging domain, Anker was the first to commercialize gallium nitride (GaN) technology globally, driving industry-wide fast-charging innovation. The Anker Prime series, powered by GaNPrime 2.0 technology, delivers "the world's most compact 160W multi-port charger." In smart security, the eufy NVR S4 Max ranked first in its category in the UK market and second in the US. In smart audio, the soundcore AeroFit 2 AI Assistant integrates AI capabilities supporting translation across 100+ languages.

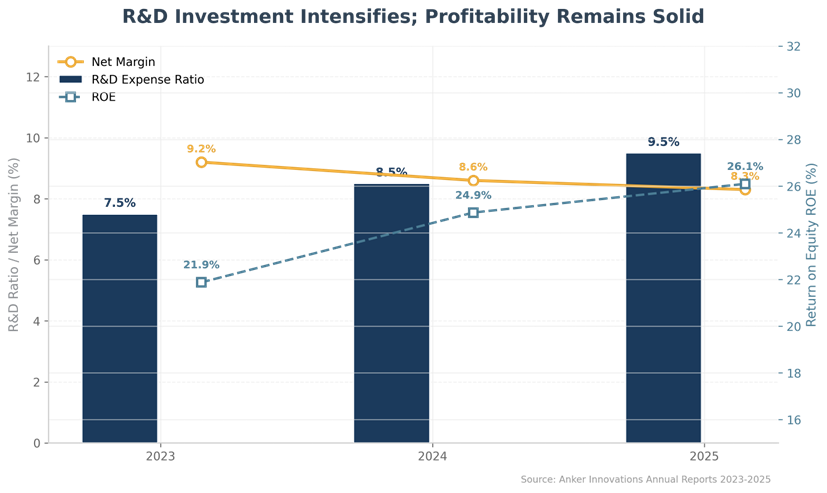

In 2025, net profit attributable to shareholders reached RMB 2.545 billion, up 20.37% YoY; basic earnings per share were RMB 4.77, up 19.47%. Weighted average ROE improved to 26.10%, up 1.23 percentage points from 2024, reflecting enhanced shareholder returns.

The company continues to intensify R&D investment. 2025 R&D expenses reached RMB 2.893 billion, with the R&D expense ratio increasing from 7.5% in 2023 to 9.5%. The company's proprietary plug-in programming system now exceeds 50% code adoption rate, and the AIME agent platform has been deployed to democratize AI capabilities across non-technical functions. This sustained R&D intensity is the key foundation for Anker's technology leadership.

Figure 3: Profitability and R&D Investment Trends 2023-2025

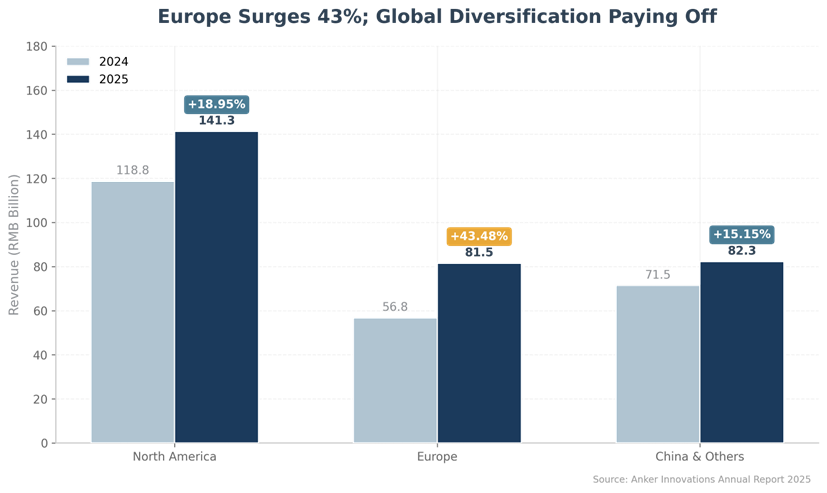

Anker Innovations maintains a global operations footprint, with overseas revenue accounting for 96.62% of total revenue in 2025. North America generated RMB 14.133 billion, up 18.95% YoY and representing 46.31% of revenue, remaining the largest market. Europe surged to RMB 8.151 billion, up 43.38% YoY, becoming the fastest-growing region. China and other markets contributed RMB 8.231 billion, up 15.15%.

Figure 4: Regional Revenue Comparison 2024-2025 (RMB Billion)

Europe's explosive growth was driven by two factors: first, strong demand for Anker SOLIX energy storage products amid Europe's energy transition; second, deepened offline channel penetration, with products now available at major retailers including Argos and OBI. While North America's growth moderated, the market fundamentals remain solid, with strengthened relationships at Walmart, Best Buy, Target, and Costco.

The company continues advancing its "online + offline" omni-channel diversification strategy. In 2025, online channels generated RMB 21.427 billion, up 21.74% YoY; offline channels achieved RMB 9.087 billion, up 27.81% YoY, with offline growth outpacing online, demonstrating effective channel synergy.

Notably, dependence on Amazon continues to decline. Amazon's revenue share dropped from 57.1% in 2023 to 52.3% in 2025, while independent sites and third-party platforms grew faster. Official website revenue grew 25.21% to RMB 3.135 billion, and other online channels (including JD.com, Shopee, and Rakuten) surged 39.20% to RMB 2.337 billion, marking substantive progress in channel diversification.

Figure 5: Channel Revenue Structure Comparison 2024-2025

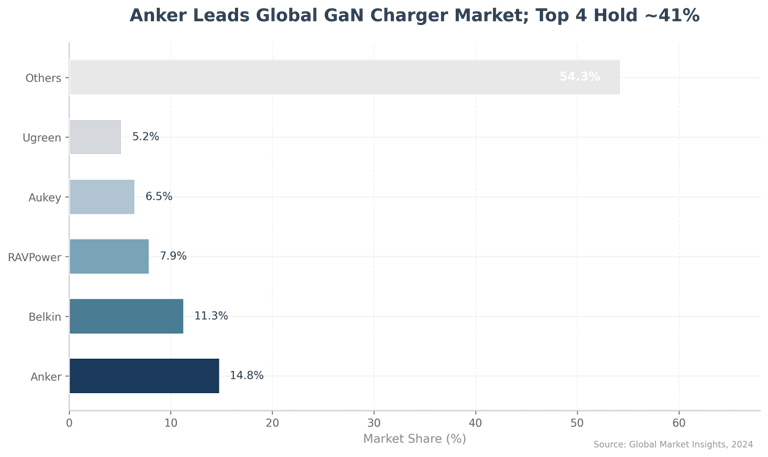

According to Global Market Insights data, in the 2024 global GaN charger market, Anker leads with a 14.8% market share. Belkin follows at 11.3%, RAVPower at 7.9%, Aukey at 6.5%, and Ugreen at 5.2%. The top four brands collectively hold approximately 40.5% market share, indicating room for further market consolidation.

Anker's leadership rests on three core advantages: first-mover advantage in GaN technology commercialization; a strong reputation for product quality and stability that creates a powerful brand moat; and a global omni-channel distribution network that far exceeds competitors' reach.

Figure 6: 2024 Global GaN Charger Market Share Distribution

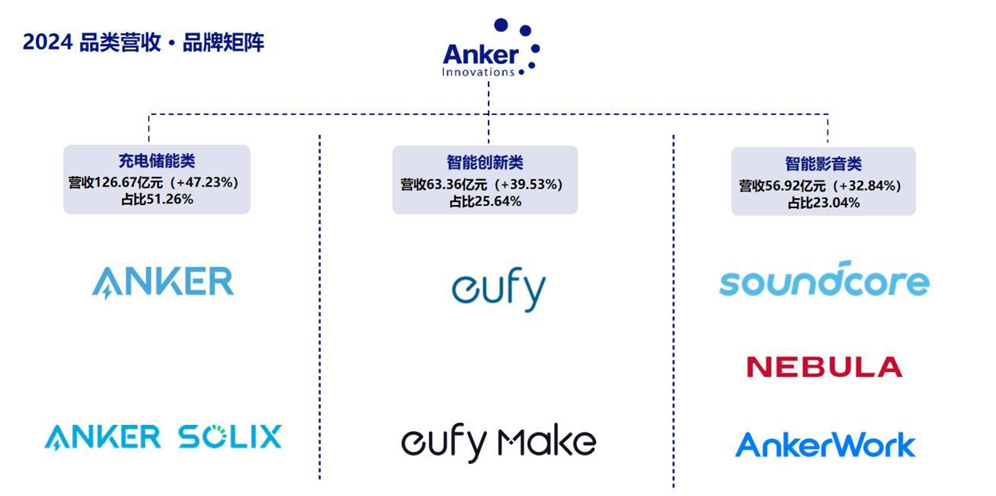

In 2025, Anker undertook a strategic consolidation of its brand architecture, reducing from four brands to three core brands: Anker covers all energy-related products, Soundcore manages audio and entertainment, and Eufy handles home automation. The projector brand Nebula was integrated under Soundcore, and the 3D printing brand AnkerMake was absorbed into the Eufy ecosystem.

|

Master Brand |

Sub-Brand |

Key Products |

Rev% |

|

Anker |

Anker / Anker SOLIX |

Chargers, power banks, energy storage |

50.5% |

|

Soundcore |

soundcore / Nebula |

Earphones, speakers, projectors |

22.4% |

|

Eufy |

eufy / AnkerMake |

Security cameras, robovacs, 3D printers |

27.1% |

This adjustment reflects the company's strategic logic of "doing many small things well." Yang categorizes companies into three types: "blue whale" firms that dominate super-categories, "great white shark" firms that deeply cultivate select categories, and "killer whale pod" firms that aggregate multiple categories. Anker's ambition is to become the third type: the Procter & Gamble or Texas Instruments of consumer electronics.

Shallow-Sea Strategy Logic

The "Shallow-Sea Strategy" operates on the premise that the consumer electronics landscape contains numerous sub-RMB-10-billion segments. While individually small, these segments can collectively build substantial scale through category innovation and channel saturation. Anker selects "shallow seas" based on two criteria: sufficient market size and the category being in an early or growth stage with room for further innovation.

The primary challenge of this strategy lies in management complexity. In 2022, the company had as many as 27 product lines, most with mediocre competitiveness; 10 product teams were subsequently closed. The company has since adopted a more focused approach, with resource allocation following a "self-sustaining"闭环 model where each product line independently generates profit, preventing the "many categories, no hits" trap.

Key Data Summary

|

Metric |

2025 Figure |

YoY Change |

|

Total Revenue |

RMB 30.514 billion |

+23.49% |

|

Net Profit |

RMB 2.545 billion |

+20.37% |

|

Weighted Avg ROE |

26.10% |

+1.23ppt |

|

R&D Expense |

RMB 2.893 billion |

+37.2% |

|

GaN Market Share |

14.8% (Global #1) |

- |

|

Amazon Share |

52.3% |

-4.8ppt |

|

Overseas Revenue |

96.62% |

+0.2ppt |