INSTA360 Brand Report

Insta360(Amazon store front) has emerged as the dominant force in the global 360-degree camera market and a formidable challenger in the action camera segment. Founded in 2015 in Shenzhen, China, the company has transformed from a niche startup into a publicly traded technology leader with revenue approaching RMB 10 billion (USD 1.35 billion) in 2025.

Our analysis reveals a company executing a multi-pronged growth strategy: maintaining 67% global market share in 360-degree cameras, and successfully expanding into enterprise imaging solutions. The 2025 IPO on Shanghai's STAR Market raised RMB 1.9 billion, with shares surging 285% on debut, valuing the company at approximately USD 11.8 billion.

However, intensifying competition from DJI, which has entered the 360-degree camera market with aggressive pricing, coupled with declining profit margins due to strategic R&D investments, presents near-term challenges. Insta360's 2025 net profit declined 6.6% despite 74.8% revenue growth, as R&D expenditure surged 97% to RMB 1.5 billion.

|

Metric |

Finding |

|

2025 Revenue |

RMB 9.74 billion (+74.76% YoY) |

|

360° Camera Market Share |

67% globally (Frost & Sullivan) |

|

Action Camera Position |

#2 globally, 37.9% in Japan (BCN-R) |

|

IPO Valuation |

USD 11.8 billion market cap |

|

R&D Investment |

RMB 1.5 billion (15% of revenue) |

|

Key Risk |

Margin compression from competitive pricing |

Insta360 was founded in July 2015 by Liu Jingkang (JK Liu) in Shenzhen, China's technology hub. The company initially focused on smartphone-compatible 360-degree cameras before pivoting to standalone action cameras. Liu, who holds a degree from Nanjing University, developed the company's first product while in college, demonstrating an early aptitude for imaging technology.

The company officially trades as Arashi Vision Inc. on the Shanghai Stock Exchange STAR Market, completing its IPO in June 2025. The offering raised RMB 1.9 billion (USD 269.7 million), representing Shanghai's largest IPO in 17 months. Xunlei Limited holds approximately 7.8% equity interest in the company.

Insta360 operates under a dual-brand strategy, with the consumer-facing 'Insta360' brand for imaging products and the newly launched 'Antigravity' brand for drone products. The company employs over 2,180 R&D personnel, representing 55.16% of total workforce, and holds 1,120 patents globally.

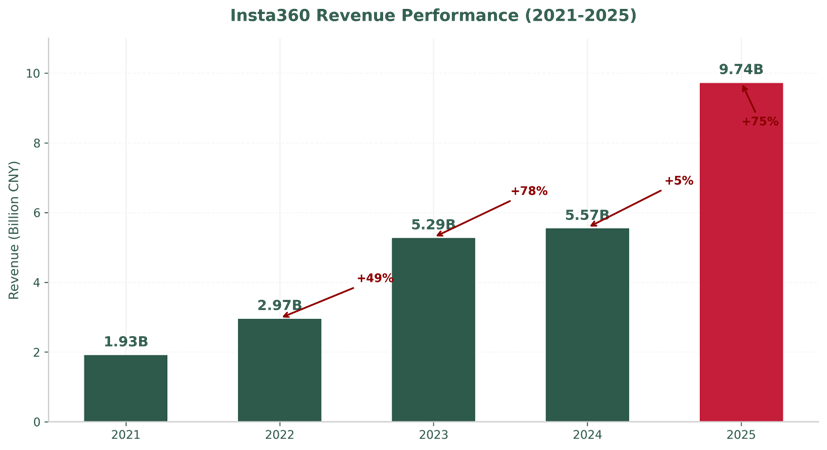

Insta360 has demonstrated exceptional revenue growth, expanding from RMB 1.93 billion in 2021 to RMB 9.74 billion in 2025, representing a compound annual growth rate (CAGR) of 49.7%. The 2025 revenue figure represents a 74.76% year-over-year increase from 2024.

Figure 1: Insta360 Revenue Performance (2021-2025) - Revenue in Billion CNY

Despite robust top-line growth, profitability has come under pressure. Net profit attributable to parent company was RMB 929 million in 2025, down 6.62% YoY. The profit decline is primarily attributable to strategic investments in chip customization, drone development, and AI integration. Gross margin compressed to 45.74% from higher levels in prior years.

The first quarter of 2026 showed continued revenue momentum (RMB 2.48 billion, +83.11% YoY) but further profit pressure (net profit of RMB 84.6 million, -52.02% YoY). The company explicitly adopted a strategy of 'sacrificing short-term profits to build long-term technological barriers,' as stated by founder Liu Jingkang in his first letter to shareholders.

|

Year |

Revenue (B RMB) |

Growth |

Net Profit (M RMB) |

Margin |

|

2021 |

1.93 |

- |

266 |

13.8% |

|

2022 |

2.97 |

+53.9% |

407 |

13.7% |

|

2023 |

5.29 |

+78.1% |

830 |

15.7% |

|

2024 |

5.57 |

+5.3% |

995 |

17.9% |

|

2025 |

9.74 |

+74.8% |

929 |

9.5% |

The global action camera market was valued at approximately USD 7.97 billion in 2025 and is projected to reach USD 26.73 billion by 2035, growing at a CAGR of 12.95%. North America leads with 34% market share, followed by Asia-Pacific at 31% and Europe at 27%. Key growth drivers include increasing participation in adventure sports, rising content creation on social media platforms, and technological advancements in stabilization, resolution, and AI-powered features.

The market is undergoing significant transformation, with Chinese manufacturers (DJI and Insta360) displacing the once-dominant American company GoPro. According to BCN-R Japan data from January 2025, GoPro's market share in Japan — historically its strongest market — has plummeted to 18.9%, down from over 75% in May 2023. DJI commands 40.1% and Insta360 holds 37.9%, together capturing nearly 78% of the market.

The intelligent imaging market has evolved into a duopoly between two Shenzhen-based companies headquartered just 10 kilometers apart: DJI and Insta360. The competition intensified in 2025 when Insta360 launched its Antigravity drone brand, directly challenging DJI's core market. DJI responded by launching the Osmo 360 panoramic camera, encroaching on Insta360's stronghold.

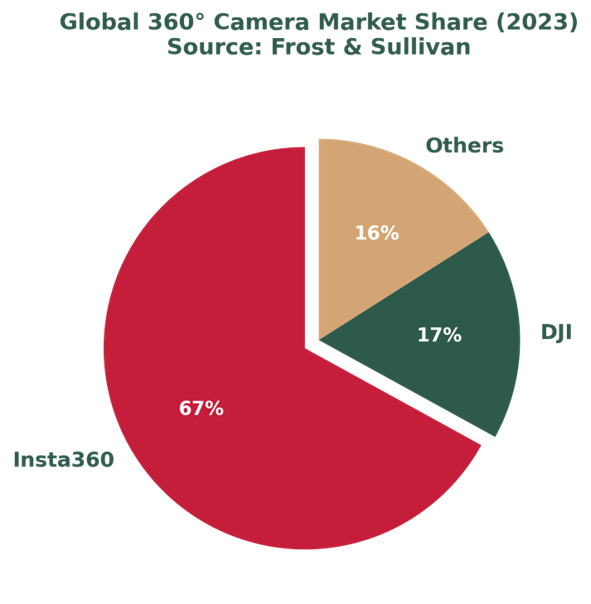

In the 360-degree camera segment, Insta360 maintains dominant market leadership with 67% global market share according to Frost & Sullivan data. DJI holds approximately 17% with its Osmo 360 product, while other players including Ricoh and GoPro share the remaining 16%.

Figure 2: Global 360-Degree Camera Market Share (2023)

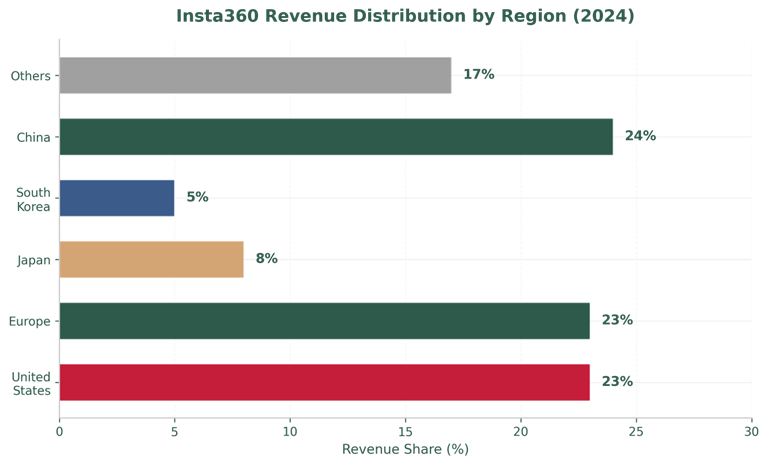

Insta360's revenue is globally diversified, with 76% derived from overseas markets. The United States and Europe each contribute 23% of revenue, followed by China at 24%, Japan at 8%, South Korea at 5%, and other markets at 17%. This geographic distribution mitigates single-market risk while positioning the company to capture growth across multiple regions.

Figure 4: Insta360 Revenue Distribution by Region (2024)

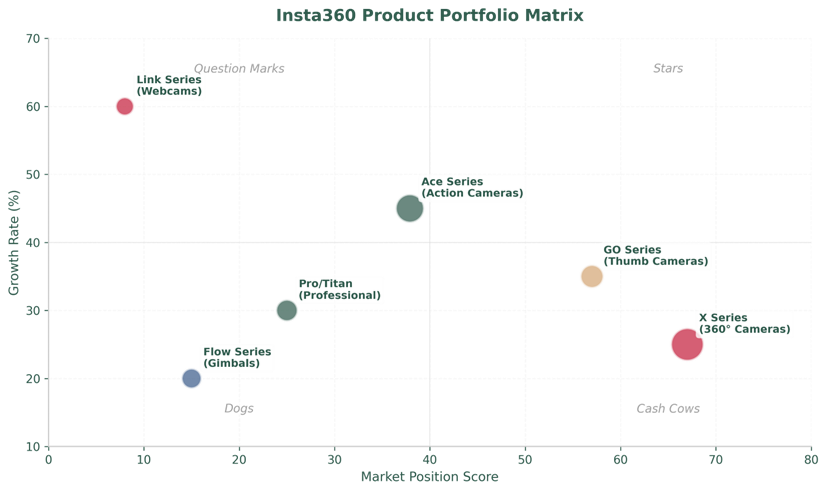

Insta360's consumer product strategy centers on comprehensive coverage of all imaging scenarios, from professional filmmaking to casual social media content. The product architecture spans six major series:

• X Series (360-degree cameras): Flagship panoramic cameras including X5, X4, and X4 Air. The X5 launched in July 2025 with 8K resolution capability, maintaining Insta360's leadership in the 360-degree segment.

• Ace Series (Action cameras): Premium action cameras co-engineered with Leica optics, featuring the Ace Pro 2 with dual AI chips and 8K recording. Positioned as direct competitors to GoPro HERO and DJI Osmo Action series.

• GO Series (Thumb cameras): Ultra-compact wearable cameras including GO Ultra and GO 3S, designed for POV capture. Japan shows the highest per-capita adoption of this series, reflecting demand for discreet, portable devices.

• Flow Series (Stabilizers): AI-powered smartphone gimbals with advanced tracking capabilities and Apple DockKit integration.

• Link Series (Webcams): AI-powered 4K webcams targeting the remote work and livestreaming market, projected to reach USD 250 billion by 2027.

The B2B segment, while currently representing approximately 20% of revenue, is growing at 25% year-over-year and offers higher-margin opportunities. Key professional products include:

• Titan & Pro Series: Cinema-grade 360-degree cameras for VR content production, real estate virtual tours, and Google Street View integration.

• Conferencing Ecosystem: Insta360 Link 2 Pro, Connect dual-camera videobar, and Wave speakerphone — forming a complete AI-powered meeting room solution certified for Zoom Rooms.

• Antigravity Drones: The A1 drone, launched in July 2025, features 360-degree capture capability and foldable design. Though initial volumes remain modest, the drone represents Insta360's strategic entry into DJI's core market.

Figure 5: Insta360 Product Portfolio Matrix - Market Position vs. Growth Rate