POP MART Analysis Report

Pop Mart(Amazon store front) International Group has emerged as the dominant force in the global designer toy market, transforming from a Beijing-based variety store in 2010 into a USD 27 billion market cap phenomenon. The company's 2024 results represent an inflection point: revenue doubled to RMB 13.0 billion (USD 1.8 billion), with overseas sales surging 375% to comprise 38.9% of total revenue, up from just 9.8% two years prior.

The investment thesis rests on three structural pillars:

(1) a proprietary IP portfolio where artist-created characters account for 85.3% of revenue with THE MONSTERS (Labubu) franchise alone generating RMB 3.0 billion; (2) a multi-channel distribution network spanning 130 international stores, 2,300 RoboShops, and rapidly scaling e-commerce; and (3) a consumer value proposition built on emotional connection rather than functional utility, commanding gross margins of 66.8% and expanding net margins toward 30%.

Our analysis suggests Pop Mart is at the early stages of global penetration. H1 2025 results validate this trajectory: revenue grew 204% year-over-year to RMB 13.9 billion, with the Americas surging 1,142% and Europe up 729%. The key strategic question is whether the company can sustain its IP innovation engine while scaling operations across culturally diverse markets.

Key Metrics at a Glance

|

Metric |

FY2022 |

FY2023 |

FY2024 |

H1 2025 |

|

Revenue

(RMB B) |

4.62 |

6.30 |

13.04 |

13.88 |

|

Gross

Margin |

57.5% |

61.3% |

66.8% |

70.3% |

|

Overseas

Mix |

9.8% |

16.9% |

38.9% |

~48% |

|

Store

Count (Int'l) |

43 |

80 |

130 |

~160 |

|

Market Cap

(USD B) |

3.5 |

3.4 |

15.4 |

27.1 |

Founded in 2010 by Wang Ning, Pop Mart began as an offline "trendy variety store" in Beijing, struggling to differentiate amid the rise of e-commerce. The pivotal moment came in 2015 when Wang drew inspiration from Japan's gachapon culture and introduced blind box mechanics to the Chinese market, combining mystery packaging with high-quality artist-designed collectible figures. This format transformation redefined the company from a retailer into a cultural platform.

The blind box model taps into deep psychological drivers: anticipation, collection completion, and social sharing. Each themed series contains common, rare, and "secret" figures with odds typically set at 1:72 or 1:144, creating scarcity-driven demand. Unlike traditional toys targeting children, Pop Mart's core demographic consists of Gen Z and Millennial consumers, predominantly female, who view these collectibles as lifestyle accessories and emotional anchors rather than playthings.

Pop Mart operates a distinctive IP development ecosystem. The Pop Design Centre (PDC) discovers artists through competitions and social media scouting, then incubates characters through a rapid prototyping and market testing process. The company collaborates with over 350 artists, with 28 under exclusive or proprietary agreements. This pipeline has produced iconic characters including Molly (debuted 2016), DIMOO, SKULLPANDA, and the breakout star THE MONSTERS (Labubu).

The company listed on the Hong Kong Stock Exchange in December 2020 (Stock Code: 9992) at HKD 38.50 per share. After a volatile post-IPO period, the stock has appreciated dramatically, reaching a market capitalization of approximately HKD 249 billion (USD 32 billion) by end-2025, reflecting investor confidence in the global expansion narrative.

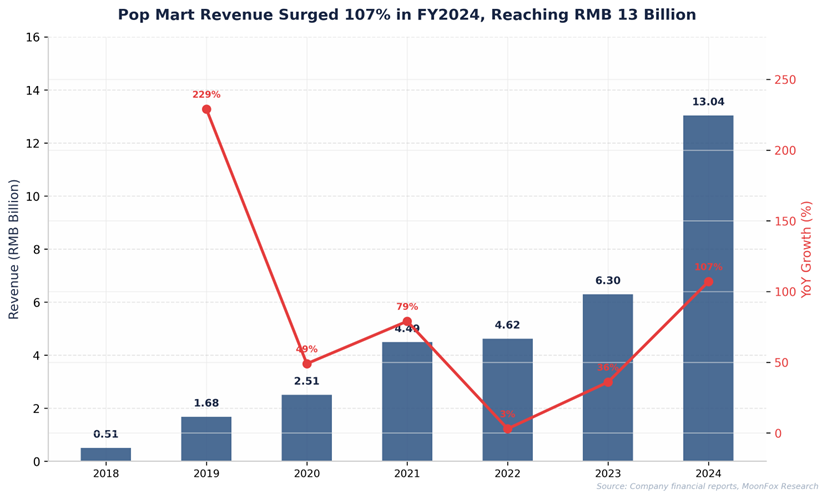

Pop Mart's financial trajectory demonstrates the power of compounding growth in an IP-driven business. From RMB 515 million in 2018, revenue has compounded at a 68% CAGR to reach RMB 13.04 billion in 2024. The 107% year-over-year growth in FY2024 represents an acceleration from the 36% recorded in 2023, driven primarily by the Labubu phenomenon and international market penetration.

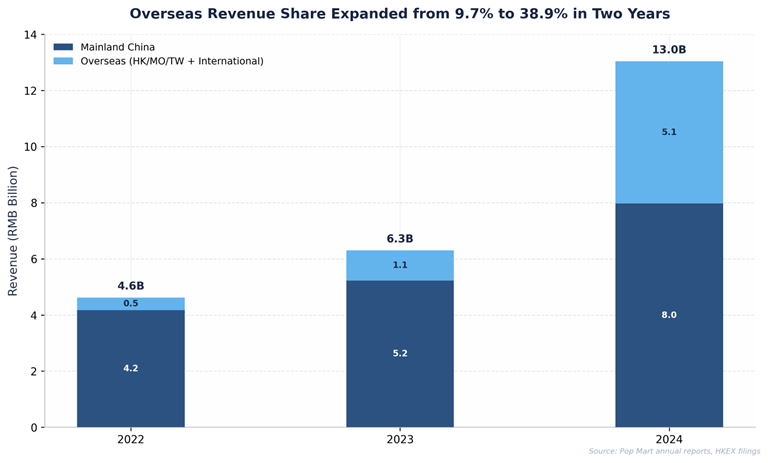

The composition of growth has shifted meaningfully. Domestic China revenue grew 52% to RMB 7.97 billion, while overseas markets exploded 375% to RMB 5.07 billion. This geographic rebalancing reduces dependence on a single market and exposes Pop Mart to higher-spending developed market consumers. Notably, H1 2025 saw overseas revenue contribution reach approximately 48%, suggesting the company may achieve true geographic parity within 12-18 months.

Figure 1: Revenue doubled in FY2024 to RMB 13.0 billion, with overseas contribution rising sharply

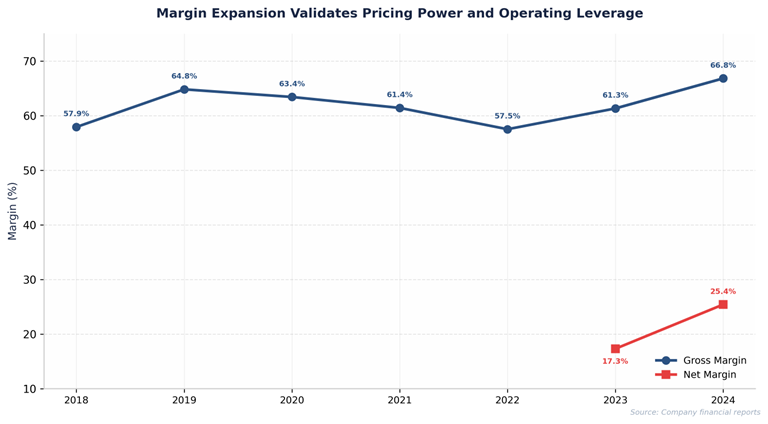

Profitability metrics validate the quality of Pop Mart's growth engine. Gross margin expanded from 61.3% in 2023 to 66.8% in 2024, reflecting both pricing power from surging demand and favorable product mix shift toward higher-margin plush items and premium MEGA collectibles. Net margin improved from approximately 17% to 25%, with H1 2025 indicating further expansion toward 30%.

This margin profile compares favorably against traditional toy manufacturers (Hasbro: ~7%, Mattel: ~10%) and even exceeds Funko's 15% net margin. The structural advantage lies in Pop Mart's owned-IP model: unlike licensed-IP businesses that pay royalties of 10-15% to IP owners, Pop Mart's artist IPs generate revenue with minimal ongoing royalty obligations, having acquired commercial rights through upfront payments or revenue-sharing agreements with creators.

Figure 2: Overseas revenue surged from 9.7% (2022) to 38.9% (2024) of total sales

Figure 3: Gross margin reached 66.8% in 2024, with net margin expanding to 25%+

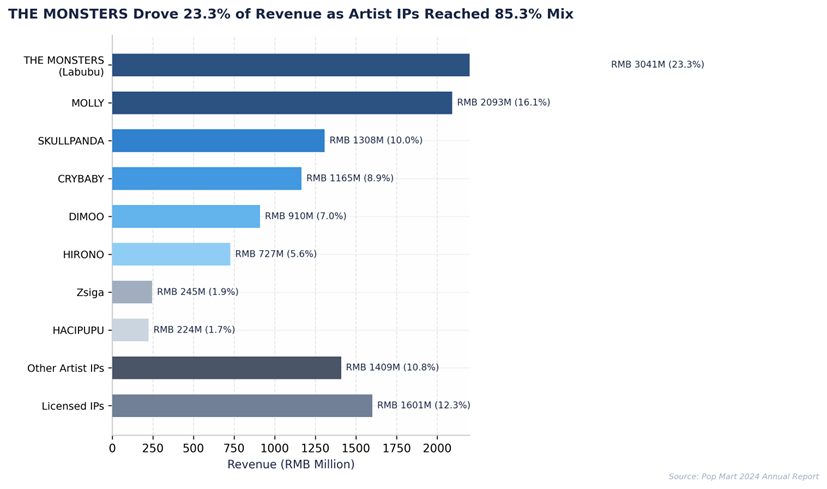

Pop Mart's competitive moat is fundamentally rooted in its IP portfolio. In 2024, artist-created IPs accounted for 85.3% of revenue (RMB 11.1 billion), while licensed IPs contributed 12.3%. This contrasts sharply with competitors like MINISO, which relies primarily on licensed third-party IP. The proprietary model delivers superior economics and brand differentiation.

THE MONSTERS series, featuring the Labubu character created by Hong Kong artist Kasing Lung, has become the company's flagship IP, generating RMB 3.04 billion (23.3% of total revenue) in 2024, up from just RMB 368 million in 2023. The Labubu character gained global virality through social media, with celebrity endorsements from figures like Lisa of BLACKPINK accelerating international awareness. The character's distinctive design, cute appearance, and emotional resonance have transcended cultural boundaries.

Critically, Pop Mart manages IP portfolios with discipline to extend lifecycle value. The company has reduced new series launches from 5-6 per year to 3-4 per major IP, avoiding consumer fatigue. SKULLPANDA, for example, took two years from artist signing to market launch, with its debut series enjoying a two-year lifecycle, far exceeding the industry average of 9-12 months. For mature IPs like Molly, Pop Mart releases only 1-2 new series per quarter, sustaining anticipation and collectibility.

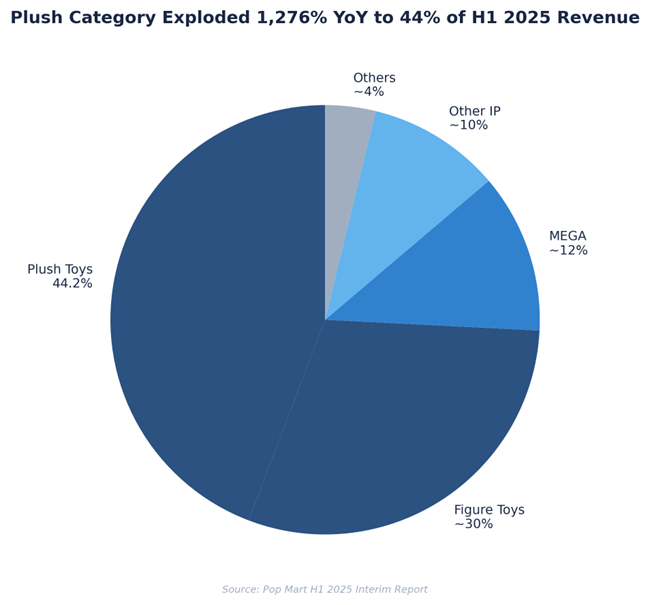

Product category expansion represents a significant growth vector. Plush toys emerged as the breakout category in 2024, with revenue surging 1,276% year-over-year in H1 2025 to comprise 44.2% of total sales. The soft, tactile nature of plush products resonates particularly strongly with international consumers and has become the preferred entry point for new collectors. The MEGA premium line, featuring larger and more detailed figures at higher price points, has also gained traction among serious collectors.

Figure 4: Artist IPs dominate revenue at 85.3%, with THE MONSTERS franchise leading at RMB 3.0 billion

Figure 5: Plush toys exploded to 44.2% of H1 2025 revenue, reshaping the product portfolio

Pop Mart's international expansion has accelerated dramatically, transforming from a China-centric business to a genuinely global brand. The company entered its first overseas market (South Korea) in 2018, and by end-2024 operated 130 retail stores and 192 RoboShops across 100 countries. Key flagship locations include the Louvre in Paris, Oxford Street in London, and premium shopping districts across Southeast Asia.

Southeast Asia has emerged as the most successful expansion region, contributing approximately 75% of overseas revenue in 2024. Cultural affinity with cute aesthetics, strong Chinese cultural influence, and Pop Mart's early-mover advantage in markets like Thailand, Vietnam, and the Philippines have driven exceptional performance. The company has established themed stores, including a CRYBABY store in Thailand and a K-POP themed location in South Korea, demonstrating localization sophistication.

Western markets present both the greatest opportunity and the steepest challenge. The Americas grew 1,142% in H1 2025, albeit from a low base, with store count expanding from 10 to 41. Europe grew 729% with stores increasing from 9 to 18. TikTok and social media virality have proven more effective than traditional marketing in building Western brand awareness, with the Pop Mart app briefly topping the U.S. App Store shopping chart in April 2025.

Supply chain localization is underway to support global growth. Pop Mart has established manufacturing facilities in Vietnam and is exploring production in Mexico to serve the North American market, reducing logistics costs and tariff exposure. This operational evolution marks the transition from an export-oriented Chinese company to a genuine multinational with distributed production capabilities.

Global Store Network Expansion

|

Year |

Stores |

RoboShops |

New Markets |

Key Locations |

|

2020 |

1 |

- |

South

Korea |

- |

|

2021 |

7 |

9 |

Singapore,

SE Asia |

- |

|

2022 |

43 |

120 |

UK, USA,

Australia |

- |

|

2023 |

80 |

159 |

France,

Thailand |

- |

|

2024 |

130 |

192 |

Italy,

Spain, Philippines |

Louvre,

Oxford St |

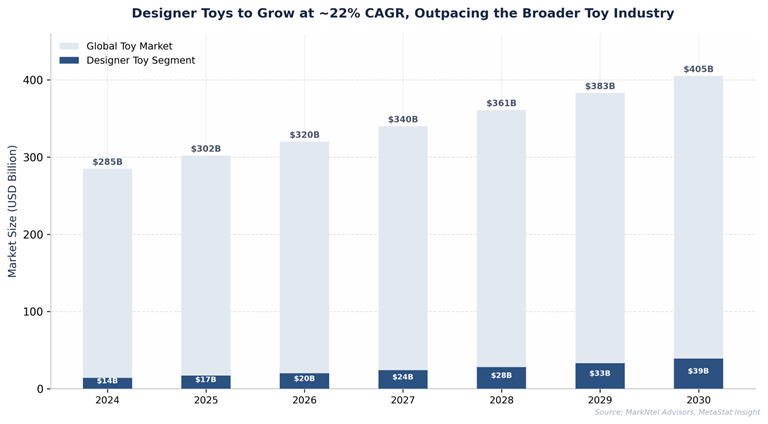

The global toy market was valued at approximately USD 285 billion in 2024 and is projected to reach USD 405 billion by 2030, growing at a 6% CAGR. Within this expansive market, the designer toy and art collectible segment, Pop Mart's core addressable market, represents an estimated USD 14 billion, growing at approximately 16-22% annually, significantly outpacing the broader industry.

Pop Mart holds the leading position in China's designer toy market with an estimated 8.3% share in 2022, and has likely expanded this significantly given recent growth. Globally, the company competes with Funko (USD 1.1 billion revenue, Pop culture vinyl figures), Medicom Toy's BE@RBRICK (luxury art toys), Mighty Jaxx (digital-physical hybrids), and increasingly MINISO's TOPTOY chain, which had 276 stores generating RMB 980 million by end-2024.

The competitive differentiation is clear: Funko relies on licensed mainstream entertainment IP, making it dependent on Hollywood and subject to royalty costs. BE@RBRICK targets ultra-high-end collectors with limited mass-market appeal. MINISO/TOPTOY competes on price (USD 5-7 vs Pop Mart's USD 12-18) but lacks original IP depth and brand premium. Pop Mart's owned-IP model, artist collaboration network, and brand positioning at the intersection of art, fashion, and collectibles create a defensible market position.

Figure 6: The designer toy segment (16-22% CAGR) significantly outpaces the broader toy industry (6% CAGR)

Competitive Positioning Matrix

|

Company |

Positioning |

Est. Share |

Key Differentiator |

|

Pop Mart |

Designer

toys / blind boxes |

8-12% |

Owned IP

portfolio, artist network |

|

Funko |

Pop

culture vinyl |

~30% |

Mainstream

licensing, mass distribution |

|

BE@RBRICK |

Luxury art

toys |

~20% |

Premium

partnerships, limited editions |

|

TOPTOY

(MINISO) |

Value

designer toys |

~5% |

Low price

point, rapid store expansion |

|

Mighty

Jaxx |

Digital-physical

hybrid |

~3% |

NFT

integration, tech-forward |