xTool Brand Research Report

xTool(Amazon store front)has emerged as the dominant global brand in consumer-grade laser engraving and cutting equipment, commanding a 47% market share by GMV in the laser engraver segment as of September 2025. Founded in 2021 as a strategic pivot from STEAM educational robotics company Makeblock, xTool has achieved remarkable growth: revenue surged from RMB 1.46 billion in 2023 to RMB 2.48 billion in 2024, representing 70% year-over-year growth.

The company's success is built on three pillars: (1) superior product performance at competitive prices enabled by China's supply chain advantages; (2) a deeply integrated hardware-software ecosystem featuring AI-powered material recognition and the proprietary xTool Studio platform; and (3) a DTC-first go-to-market strategy that drives 61% of revenue through its official website while maintaining exceptional customer loyalty with a 40% repurchase rate and NPS of 67.

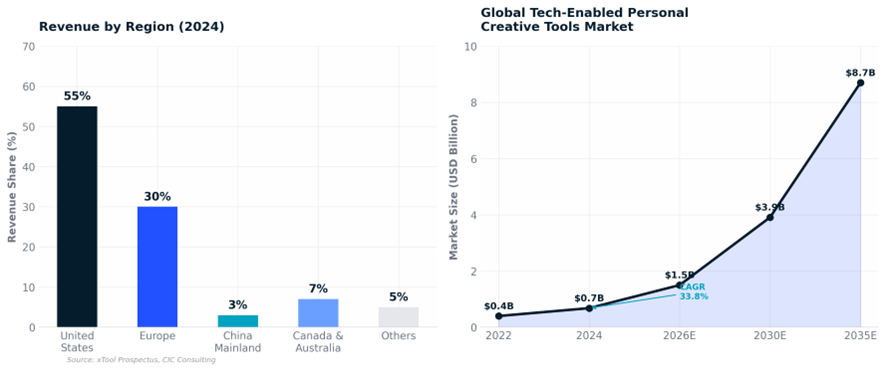

With 97% of revenue generated from overseas markets (primarily the United States at 55% and Europe at 30%), xTool exemplifies the "R&D in China, sales worldwide" model. The company filed for IPO on the Hong Kong Stock Exchange in January 2026, with a pre-IPO valuation of USD 1.1 billion following a USD 200 million Series D round led by Tencent.

xTool operates under Maker Works Technology Co., Ltd., formerly known as Makeblock, which was founded in 2013 by Jasen Wang. The original Makeblock business focused on STEAM education robotics, serving over 25,000 schools across 140 countries. However, the COVID-19 pandemic and China's "double reduction" education policy severely impacted the education technology sector, leading to annual losses exceeding RMB 10 million.

In 2020, Wang and his team identified a significant gap in the overseas market for accessible, consumer-grade laser devices among DIY enthusiasts and makers. This insight prompted a decisive pivot: the xTool brand was officially launched in 2021 with the xTool D1, its first semiconductor laser engraver. The company's first Kickstarter campaign for the xTool M1 raised USD 2.6 million, becoming the top-funded laser project on the platform that year.

Today, xTool has evolved into a comprehensive creative tools platform with over 405,000 connected devices worldwide as of September 2025. The company maintains dual manufacturing facilities in China and Thailand, with R&D headquartered in Shenzhen and international operations supported by offices in California and Berlin.

Jasen Wang (Wang Jianjun), founder and CEO, is a Northwestern Polytechnical University graduate and robotics enthusiast who has been recognized by Forbes China as one of its "30 Under 30" top entrepreneurs. Wang's maker movement roots and product-centric philosophy have shaped xTool's mission to lower the barriers to creation while expanding creative boundaries. Under his leadership, the company transitioned from a B2B education robotics provider to a global DTC consumer technology brand in under five years.

The global market for technology-enabled personal creative tools is experiencing explosive growth. According to CIC Consulting, this market is expected to expand from USD 6.8 billion in 2024 to USD 39.1 billion by 2030, representing a compound annual growth rate (CAGR) of 33.8%. Within this broader category, laser-based personal creative tools represent one of the fastest-growing segments, projected to grow from USD 0.4 billion in 2022 to USD 7.9 billion by 2035.

The laser engraving equipment market specifically is valued at approximately USD 9.6 billion in 2024 (encompassing both consumer and commercial grades), with a projected CAGR of 18.9% through 2030. Key growth drivers include: the rising maker movement and DIY culture, particularly in North America and Europe; increasing demand for personalized products and small-batch customization; declining hardware costs due to supply chain maturation; and AI-powered software that dramatically reduces the learning curve for new users.

Figure 1: Regional Revenue Distribution (Left) and Global Market Projection (Right)

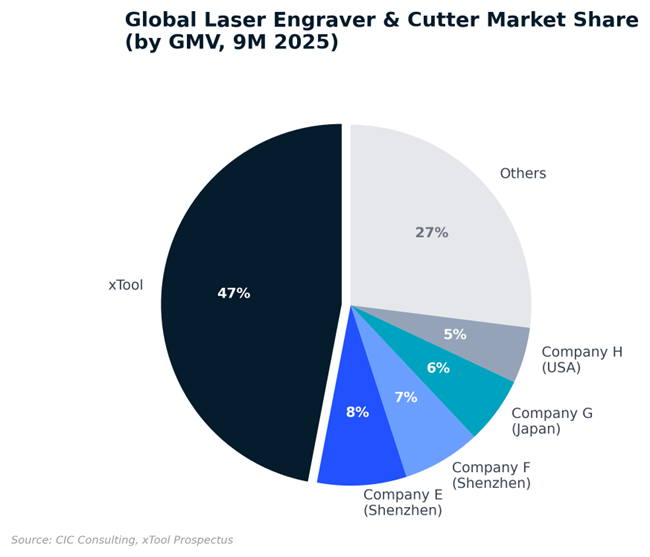

xTool holds a commanding market position in the global consumer laser engraving landscape. In 2024, xTool captured 42.8% of the laser engraver and cutter market by GMV, making it the largest brand worldwide. By the first nine months of 2025, this share had grown to 47% in the laser engraver segment alone, approximately six times that of the second-ranked competitor and exceeding the combined share of brands ranked second through tenth.

The competitive landscape features three distinct tiers: premium professional manufacturers (Epilog Laser, Trotec, Universal Laser Systems), mid-market challengers (Glowforge, OMTech, Thunder Laser), and value-oriented Chinese DTC brands (Ortur, Atomstack, LaserPecker). xTool has successfully carved out a unique position bridging the mid-market and premium tiers, offering professional-grade capabilities at prices 10-30% below comparable competitors.

Figure 2: Global Laser Engraver and Cutter Market Share by GMV (9M 2025)

The following table provides a comparative assessment of xTool against its key competitors across critical dimensions:

|

Dimension |

xTool |

Glowforge |

Atomstack |

LaserPecker |

|

Avg.

Price |

10-30%

Premium |

Premium |

Budget |

Mid-range |

|

Software |

Free

(XCS) |

$50/month |

Basic |

App-based |

|

Market

Share |

47%

(#1) |

Declining |

Growing |

Niche |

|

Product

Range |

Broad |

Narrow |

Mid-range |

Portable |

|

Offline

Presence |

300+

showrooms |

Limited |

None |

Limited |

Table 1: Competitive Comparison Matrix

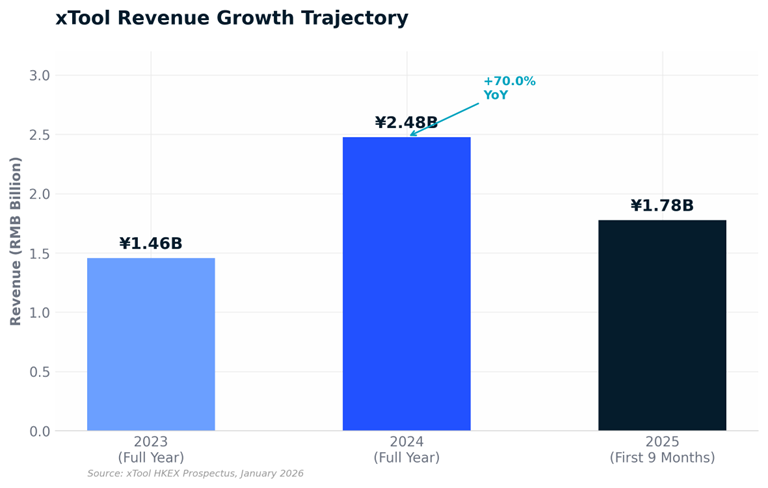

xTool's financial trajectory demonstrates exceptional growth. Revenue increased from RMB 1.46 billion in 2023 to RMB 2.48 billion in 2024, representing 70% year-over-year growth. In the first nine months of 2025, revenue reached RMB 1.78 billion, up 18.6% compared to the same period in 2024. This moderation in growth rate reflects both a larger revenue base and a strategic shift toward higher-margin, premium products.

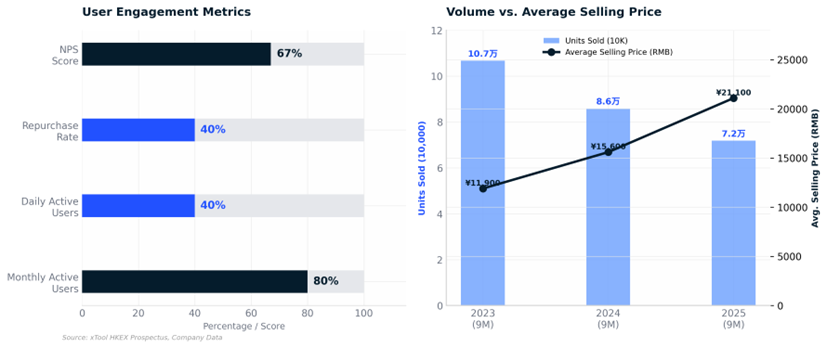

A notable trend is the "rising price, falling volume" dynamic: unit sales decreased from 85,900 units in 9M 2024 to 71,900 units in 9M 2025, while the average selling price increased from RMB 15,600 to RMB 21,100. This indicates successful execution of a premiumization strategy, with higher-end models (P2, F1 Ultra, M1 Ultra) driving revenue growth while the company strategically cedes the entry-level segment to budget competitors.

Seasonality significantly impacts xTool's performance, with Q4 (encompassing Black Friday and Cyber Monday) contributing disproportionately to annual revenue. During the 2025 Black Friday period, xTool achieved single-day GMV exceeding RMB 100 million for the first time, with overall promotion-period GMV increasing approximately 50% year-over-year.

Figure 3: xTool Revenue Growth Trajectory (2023-2025)

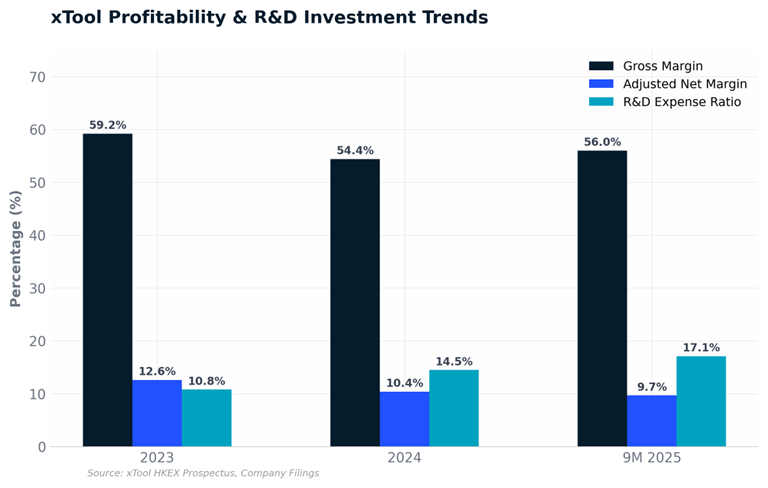

xTool maintains strong gross margins characteristic of premium consumer technology brands. Gross margin has remained stable in the 54-59% range, reaching 56.0% in 9M 2025. This margin profile reflects the company's pricing power and supply chain efficiencies: material costs account for only approximately 30% of operating revenue, while the gross profit margin of ~55% is closer to consumer goods than industrial equipment.

However, the company operates with thin net margins due to heavy investments in growth. Reported net profit margin was 7.6% in 2023, 6.0% in 2024, and 4.7% in 9M 2025. Adjusted net profit margins (non-IFRS) were more stable at 12.6%, 10.4%, and 9.7% respectively. R&D expense ratio increased significantly from 10.8% in 2023 to 17.1% in 9M 2025, reflecting intensified investment in AI capabilities and new product categories.

Sales and marketing expenses represent the largest cost category after COGS, at 22.6% of revenue in 9M 2025. Marketing and advertising expenses rose from RMB 216 million in 2023 to RMB 314 million in 2024, while promotion fees paid to third-party platforms increased from RMB 133 million to RMB 176 million. Customer acquisition costs are rising, reflecting intensifying competition for traffic in the consumer laser equipment market.

Figure 4: xTool Profitability and R&D Investment Trends

xTool's product ecosystem spans multiple laser technologies and use cases, organized into three main categories: laser engravers and cutters (the core business), laser welding machines and CNC cutters, and material printers. The company offers products across all major laser types: diode lasers (entry-level to mid-range), CO2 lasers (professional-grade cutting), and fiber lasers (metal marking and industrial applications).

The flagship P2 series features a 55W CO2 laser capable of cutting 18mm walnut or 20mm acrylic in a single pass with 0.08mm precision. The F1 Ultra employs dual 20W fiber lasers achieving engraving speeds of 10,000 mm/s. The M1 Ultra integrates four functions: laser engraving, blade cutting, inkjet printing, and pen drawing, serving as an all-in-one creative workstation. In June 2025, xTool launched its first DTF (Direct to Film) garment printer, capturing 12.7% of the global DTF market within months and ranking third worldwide by GMV.

Figure 5: Competitive Product Positioning: Price vs. Laser Power

xTool's competitive moat is fundamentally rooted in software and algorithmic capabilities rather than hardware manufacturing alone. The company has developed its proprietary xTool Studio (XCS) software platform, which integrates AI-powered material recognition that automatically configures optimal parameters for over 20 materials including wood, leather, and acrylic. According to company data, this AI feature reduces the learning curve by approximately 60%.

The AIMake creative intelligent agent enables users to generate product designs through natural language prompts, which can then be refined in xTool Studio and executed directly on connected machines. This creates a seamless closed-loop workflow from ideation to physical production. As of September 2025, xTool held hundreds of patents and trademarks in China and overseas, with 753 R&D personnel comprising approximately 56% of total employees.

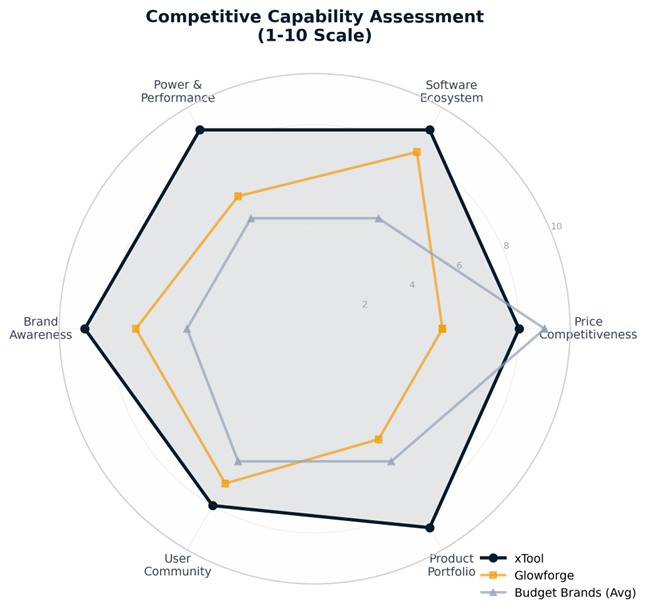

Figure 6: Competitive Capability Assessment (1-10 Scale)

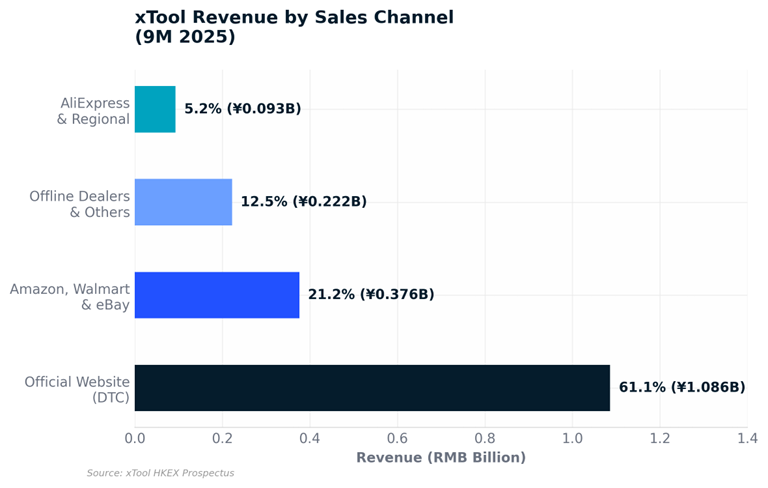

xTool operates a DTC-first omnichannel distribution strategy. In the first nine months of 2025, the company's official website (xTool.com) generated RMB 1.086 billion in revenue, accounting for 61.1% of total revenue. Third-party e-commerce platforms including Amazon, Walmart, and eBay contributed approximately RMB 376 million (21.2%), while offline dealers and other channels contributed the remaining 17.7%.

xTool DTC website

The DTC model enables xTool to maintain higher margins, control brand presentation, and capture valuable customer data. The company offers 3-day delivery in North America and after-sales response times twice as fast as competitors. Traffic to xTool's independent website reached 5.3 million visits in the three months from September to November 2025, with 77% of organic search traffic coming from branded keywords.

Figure 7: xTool Revenue by Sales Channel (9M 2025)

xTool has built a robust creator ecosystem that drives organic growth and customer retention. The company operates the Atomm online community platform with over 212,000 registered users who have shared 40,000 original works. Complementing this digital community, xTool has established the "xTool Squad" offline experience network covering 32 countries with 470 user-led sites where experienced users host demonstrations and workshops.

User engagement metrics are exceptional: approximately 80% of users operate their machines at least monthly, 40% use them daily, and the overall repurchase rate stands at 40%. The Net Promoter Score of 67 indicates strong customer satisfaction and brand advocacy. These metrics demonstrate that xTool has successfully transitioned from a transactional hardware vendor to a platform-based creative community.

Figure 8: User Engagement Metrics (Left) and Volume vs. ASP Trend (Right)

The company has strategically partnered with major retail brands including Decathlon, Stanley, Ray-Ban, and PRG Golf for pop-up engraving experiences. These collaborations embed xTool devices into specific consumer scenarios (camping, sports, eyewear), allowing potential customers to experience the technology firsthand and receive personalized engravings on purchased products. This "try before you buy" approach reduces return rates while strengthening emotional attachment to the brand.

xTool's growth trajectory is supported by several structural tailwinds. First, the global maker economy and personalized customization trend continue to expand, with AI-powered software reducing barriers to creation. The company estimates that 45% of personal creative tool users first entered the category through laser engravers. Second, geographic expansion opportunities remain significant, particularly in Europe where xTool recently established a Berlin regional office and is deploying 300+ experience showrooms and 40+ service locations.

Third, category expansion into material printing (DTF/UV printers) represents a substantial addressable market increase. The global material printing market is projected to grow from USD 0.2 billion in 2024 to USD 20.4 billion by 2035. xTool's DTF printer, launched in June 2025, already captured 12.7% global market share within months, with 36% of garment printer customers being existing laser engraver users, demonstrating strong cross-selling potential.

Fourth, the content flywheel effect continues to accelerate. xTool's influencer marketing strategy encompasses 4,400+ sponsored content pieces across Instagram (54%), YouTube (30%), and TikTok (16%), with particular focus on micro-influencers (10K-50K followers) who deliver high engagement at cost-efficient rates. The brand's social media presence includes 400,000+ Instagram followers, 300,000+ TikTok followers, and 110,000+ YouTube subscribers.

Several risks merit consideration. Revenue concentration in mature markets (85% from Europe and North America) exposes xTool to economic downturns and potential trade policy changes, including tariff risks that prompted the company to establish manufacturing in Thailand. The competitive landscape is intensifying as more Chinese manufacturers enter the consumer laser segment, potentially pressuring pricing and margins.

Growth deceleration is evident: revenue growth slowed from 70% in 2024 to 18.6% in 9M 2025. While partly attributable to a larger base and strategic premiumization, sustaining historical growth rates will become increasingly challenging. Additionally, the company's heavy reliance on marketing spend (22.6% of revenue) raises questions about the sustainability of customer acquisition costs in a more competitive environment.

Supply chain dependencies also present risk. Core components including lasers and sensors are externally sourced, with manufacturing concentrated in China and Thailand. Any disruption to these supply chains could impact production capacity. Finally, as a technology hardware company, xTool faces ongoing product obsolescence risk and must continuously innovate to maintain its market-leading position.

xTool presents a compelling investment opportunity for investors seeking exposure to the rapidly growing consumer creative tools market. The company has demonstrated exceptional execution in building a global premium brand from China, achieving market leadership with 47% share in the laser engraver segment. Its asset-light, R&D-intensive business model generates 55%+ gross margins while the DTC channel provides direct customer relationships and superior unit economics.

The IPO valuation of potentially HKD 10+ billion reflects market expectations of xTool becoming the "Insta360 of the laser industry" - a Chinese consumer technology brand that achieves global category dominance. However, investors should weigh the company's impressive growth and market position against decelerating revenue growth, thin net margins, rising customer acquisition costs, and an increasingly competitive landscape.

Key metrics to monitor include: (1) sustained gross margin stability above 50%; (2) R&D ROI measured by new product success and time-to-market; (3) DTC channel growth and customer acquisition cost trends; (4) cross-selling success in material printing; and (5) international expansion progress, particularly in Europe. The company's ability to execute its premiumization strategy while defending market share against lower-priced competitors will be critical to long-term value creation.

The following table summarizes xTool's key financial metrics:

|

Metric |

2023 |

2024 |

9M 2025 |

|

Revenue

(RMB B) |

1.46 |

2.48 |

1.78 |

|

YoY

Growth |

N/A |

+70.0% |

+18.6% |

|

Gross

Margin |

59.2% |

54.4% |

56.0% |

|

Adj.

Net Margin |

12.6% |

10.4% |

9.7% |

|

Units

Sold (10K) |

10.7 |

13.8 |

7.2 |

|

ASP

(RMB) |

11,900 |

15,900 |

21,100 |

|

R&D

Expense Ratio |

10.8% |

14.5% |

17.1% |

Table 2: xTool Key Financial Metrics Summary